AN

ANALYSIS ON ACCOUNTING EDUCATION AND NATIONAL EDUCATION POLICY RESEARCH

Ms. Deeksha Chaurasia1,

Dr. Punnam Veeriah2 Dr. Sunil S. Desai3

1Assistant

Professor, Department of Business and Commerce,

Pandit

Sunderlal Sharma Central Institute of Vocational Education (PSSCIVE), Bhopal.

2Professor

& Head Department of Business and Commerce,

Pandit

Sunderlal Sharma Central Institute of Vocational Education (PSSCIVE), Bhopal,

3Assistant Professor, Dr. Ghali

College,

Gadinglanj,

Dist. Kolhapur, Maharashtra,

ABSTRACT

Accounting education plays a crucial role

in shaping the future of finance professionals. It encompasses a wide range of

topics, including financial reporting, auditing, taxation, and management

accounting. A strong foundation in accounting principles is essential for

individuals pursuing careers in finance, auditing, consulting, and other

related fields. National education policies have a significant impact on how

accounting education is structured and delivered. These policies are formulated

by governments to outline the goals, objectives, and strategies for education

at the national level. They influence curriculum design, teaching methods,

assessment practices, and overall educational standards. The

methodology of this paper is based on primary data and secondary data. A

structured questionnaire was designed and data was collected from educators, academicians.

The data was analyzed and interpreted by applying descriptive statistics. The

study will help to analyses the impact of National Education Policy on accounting

education. The

research paper involves a systematic approach to gather information, analyze

data, and present findings.

Key

Words: National Education Policy, strong

foundation, teaching methods, educational standards

INTRODUCTION

Accounting

education refers to the formal process of learning and acquiring knowledge and

skills related to accounting principles, practices, and procedures. It is a

crucial aspect of preparing individuals for careers in accounting, finance, and

related fields. Accounting education typically starts with teaching fundamental

concepts such as double-entry bookkeeping, financial statements, and basic

accounting principles like the accrual basis of accounting. Technical Skills

provides training in the use of accounting software, spreadsheets, and other

tools necessary for recording, organizing, and analyzing financial data.

Students learn

about the various regulatory frameworks and standards that govern financial

reporting, such as Generally Accepted Accounting Principles (GAAP) and

International Financial Reporting Standards (IFRS). Emphasis is placed on

ethical considerations in accounting practice, including issues related to

honesty, integrity, and confidentiality. Accounting education often offers

specializations in areas like auditing, taxation, management accounting,

forensic accounting, and financial analysis, allowing students to focus on

specific career paths. Students are trained to analyze financial information,

identify issues, and make informed decisions based on the data available. Effective

communication of financial information, both in writing and orally, is a vital

component of accounting education. This includes preparing reports,

presentations, and financial statements. Many accounting programs are designed

to prepare students for professional certifications like Certified Public

Accountant (CPA), Chartered Accountant (CA), Certified Management Accountant

(CMA), and others. Given the evolving nature of accounting standards and

practices, accounting professionals often engage in ongoing education and

professional development to stay updated with industry changes. With the

increasing use of technology in accounting, modern accounting education often

includes training in accounting software, data analytics, and other

technological tools. Some programs incorporate experiential learning through

internships, case studies, or simulated business scenarios to give students

hands-on experience. As businesses operate in a globalized world, accounting

education may include an international perspective, considering the

implications of different accounting standards and practices around the world.

For advanced studies in accounting, research skills are emphasized, enabling

students to contribute to the body of knowledge in the field through academic

research.

Accounting

education aims to foster adaptability in graduates, recognizing that the

accounting profession is subject to continuous change. Overall, accounting

education equips individuals with the knowledge and skills needed to perform

various accounting functions, whether in public accounting firms, corporations,

government agencies, non-profit organizations, or as independent practitioners.

It serves as the foundation for a wide range of careers in finance and accounting-related

fields.

The National

Education Policy (NEP) of 2020 has a significant impact on the field of

accounting education in India. It introduces several reforms and initiatives

aimed at modernizing and enhancing the quality of accounting education. The NEP

encourages a multidisciplinary approach in higher education, allowing students

to pursue a diverse range of subjects alongside their chosen field of study,

including accounting. The policy emphasizes flexibility in course selection,

allowing students to customize their education to suit their interests and

career goals within the field of accounting. The NEP advocates for the

integration of vocational education, including specialized courses in

accounting, from the secondary level onwards. This allows students to gain

practical skills alongside academic learning. The NEP places a strong emphasis

on experiential learning, which is particularly valuable in accounting

education where practical skills are crucial. The policy promotes the use of

technology in education. In accounting, this may include training in accounting

software, data analytics tools, and other relevant technologies. The NEP

encourages research and innovation in education, which can lead to advancements

in accounting education methodologies, curriculum design, and practices. The

NEP emphasizes the importance of inculcating ethical values and professionalism

in education. In accounting, this is particularly relevant as ethical conduct

is fundamental to the profession. The policy highlights the need for continuous

training and professional development of teachers. In accounting education,

this ensures that educators stay updated with industry practices and standards.

The NEP acknowledges the importance of financial literacy and aims to integrate

it into the curriculum. This is particularly relevant in accounting education,

where understanding financial concepts is essential. The policy encourages a

global perspective in education. In accounting, this may involve studying

international accounting standards and practices. The NEP emphasizes the

development of critical thinking and problem-solving skills, which are highly

valuable in accounting where complex financial issues often require analytical

solutions. The NEP seeks to align education with the needs of the industry. In

accounting, this means preparing students for the demands of the accounting

profession and related fields.

Overall, the NEP 2020 provides a framework that

supports the modernization and enhancement of accounting education in India. It

aims to produce well-rounded accounting professionals who are equipped with not

only technical skills but also critical thinking abilities, ethical values, and

a global perspective. These changes are expected to have a positive impact on

the quality and relevance of accounting education in the country.

REVIEW OF LITERATURE

The literature review is basically a

belief on the collection of information that the researcher has learned from

others and build our own beliefs based on the work and knowledge of other researchers.

The research provides that the conclusions drawn todays researches are being

made similar efforts in past researches. Literature review by different authors

shows that they had an in-depth grasp on the key words skill development practices,

challenges, issues and prospects which are as under:

Nicholas

J. Paisey (2003) , An analysis of accounting education

research in accounting education: an international journal – 1992–2001, This report examines the research

papers published in the first 10 volumes of Accounting Education: an

international magazine since its founding in 1992, highlighting both those

areas that have been adequately addressed and those that offer prospects for

additional study. The study contrasts coverage with American accounting

education research that has been released. The document is intended to be of

interest to researchers who seek to establish the existing literature on their

study themes or who are looking for research topics and/or methodologies that

have previously gone unexplored. In order to acquire a deeper understanding of

the condition of accounting education research at the beginning of the

twenty-first century, the study also offers some insights concerning the

techniques used and the sources of the studies. Deb, P. (2020) ,

“Vision for Foreign Universities in the National Education Policy 2020: A

Critique” that deals with the internationalization of Indian higher education

as one of the stated aims of the National Education Policy (NEP) 2020. Aithal

(2020) , “Analysis of the Indian National Education Policy 2020 toward

Achieving its Objectives” and highlighted various policies announced in the

higher education system and likened them with the currently adopted system.

Various innovations and predicted implications of NEP 2020 on the Indian higher

education system along with its merits are discussed. Some suggestions are

proposed for its effective implementation towards achieving its objectives. Ponemon, Lawrence; Glazer, Alan (2021), Accounting Education and Ethical Development: The

Influence of Liberal Learning on Students and Alumni in Accounting Practice,

This study looks at the ethical growth of

undergraduate accounting students and graduates from two colleges that have

vastly different curriculum, educational philosophies, and working cultures.

Both colleges provide undergraduate accounting degrees. The study investigates

the impact of a college education and work experience on a person's ethical

development by drawing from the field of moral psychology and employing a

well-known psychometric tool called the Defining Issues Test (DIT).

RESEARCH OBJECTIVE

- To

assess the awareness of educators regarding the National Education Policy

(NEP) introduced in 2020.

- To

examine the level of understanding among educators regarding the key

provisions of the NEP,2020 as it pertains to accounting education.

- To

investigate the impact of the NEP,2020 on the quality of accounting education

in India from the perspective of educators.

- To

identify any observed changes in the curriculum or teaching methodologies

in accounting education post the implementation of NEP,2020.

- To

identify specific areas within accounting education that require further

research attention under the NEP,2020.

RESEARCH DESIGN

The

study employs a descriptive research approach, utilizing a case study

methodology. Data is collected through questionnaire with key stakeholders

involved in the Analysis on Accounting Education and National Education Policy

Research. The data is analyzed using thematic analysis to identify patterns and

themes related to the implementation process and its outcomes. Therefore, the study aims to fulfil

the parameters of analytical and descriptive research in nature.

DATA COLLECTION

Primary data is collected with the help of questionnaire

from stakeholders. Stratified Random sampling method was applied, and samples

are collected from 50 teachers/educators. Various statistical tools were

applied in this research paper. In this study, a review of

secondary sources like government reports, newspaper/ news channels, magazines

have also been used for comparing the information collected from the

respondents in primary data.

STUDY PERIOD

The study period

for data collection is from January, 2022 to October, 2023. The study was

conducted post the implementation of the National Education Policy (NEP) in

2020.

RESULT

AND ANALYSIS

For this present study the data was

collected from teacher’s, to discovery the awareness

of national education policy (NEP), impact of NEP on accounting education,

challenges and opportunities, teaching and learning methods, research and

development, recommendations and future outlook.

Section 1: Awareness of National Education Policy

(NEP)

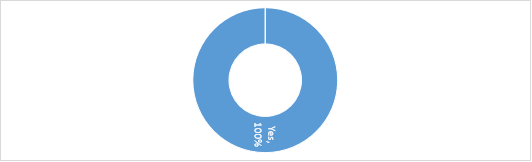

1.

Are you familiar with the National

Education Policy (NEP) introduced in 2020?

Table

No 1.1

|

|

Frequency |

Percent |

|

Yes |

50 |

100% |

|

No |

0 |

0% |

|

Total |

50 |

100% |

Figure

No 1.1

The above chart shows the

awareness of NEP,2020 among educators. I am glad to note that 100% educators

are familiar with the National Education Policy (NEP) introduced in 2020. This

shows that educators are aware what changes are been brought up in NEP,2020.

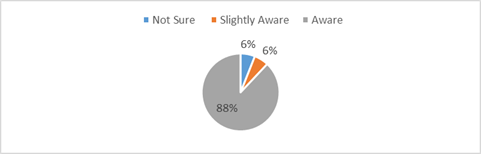

2.

How well-informed are you about the

key provisions of the NEP,2020 as it pertains to accounting education?

Table

No 1.2

|

|

Not

Aware |

Not

Sure |

Slightly

Aware |

Aware |

Total |

|

Frequency |

0 |

3 |

3 |

44 |

50 |

|

Percent |

0% |

6% |

6% |

88% |

100

% |

Figure

No 1.2

The above chart shows that how educators are well-informed

about the key provisions of the NEP,2020 as it pertains to accounting

education. 88% educators are aware about the latest change in accounting

education. 6% educators are not clear what exactly changes in NEP 2020. 6%

educators are partially aware about the accounting education.

Section 2: Impact of NEP on Accounting Education

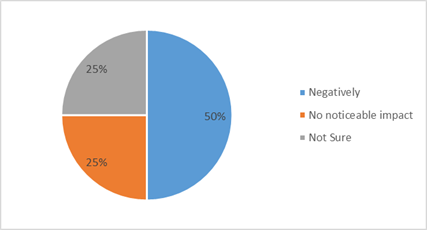

1. In

your opinion, how has the NEP,2020 influenced the quality of accounting

education in India?

Table

No 1.3:

|

|

Positively |

Negatively |

No

noticeable impact |

Not Sure |

Total |

|

Frequency |

46 |

2 |

1 |

1 |

50 |

|

Percent |

92% |

4% |

2% |

2% |

100 % |

Figure

No 1.3:

The above chart

depicts the impact of NEP in accounting Education.50% educators are in favor

that NEP,2020 influenced the quality of accounting education in India whereas

25% educators did not notice any change with the implementation of NEP.25%

educators are in negatively favor of NEP.

2. Have

you observed any changes in the curriculum or teaching methodologies in

accounting education post the implementation of NEP,2020? If yes, please

specify.

Following are the

responses received from Educators:

·

Lot of changes are required which are

Practical oriented content should incorporate, On the job training is very much

required, Internship and project based assignment will give to the students,

Activity based content should put and arrange field visits.

·

Question paper pattern is of high level

which is helpful to clear professional of exams

·

Yes, CBSE launched Competency Based

Questions that include current knowledge on business & industry

·

Yes

·

Not Yet

·

No

·

Single regulator for higher education

institutions

·

Multiple entry and exit options in degree

courses

·

Discontinuation of MPhil programs

·

Low stakes board exams

·

Common entrance exams for universities.

Section 3: Challenges and Opportunities

3. What

do you consider to be the main challenges faced by accounting education in

light of the NEP,2020?

·

First challenge facing is not getting

industrial collaboration, second appointment of trained facilities with

industrial exposure, Create interest among the stakeholders for improvement

practical aspects and availability of suitable lab equipment.

·

Vast syllabus

·

No practical experience to the students

·

Basic Accounting knowledge through

practical approach

·

Computerized Accounting system

·

Lack of Approach

·

Awareness on Commerce Education from class

IX onwards as Commerce has been suggested from class IX.

·

Alignment with NEP Goals

·

Integration of Holistic and

Multidisciplinary Education

·

Emphasis on Critical Thinking and Problem

Solving

·

Teacher Training and Professional

Development

·

Infrastructure and Technology Integration

·

Assessment and Evaluation Methods

·

Engagement with Industry and Practical

Application

·

Equity and Inclusivity

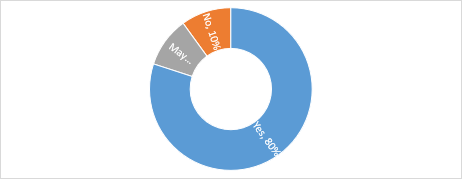

4. Are

there any new opportunities that the NEP,2020 has presented for improving

accounting education?

Table

No 1.4:

|

|

Frequency |

Percent |

|

Yes |

40 |

80% |

|

No |

5 |

10% |

|

May Be |

5 |

10% |

|

Total |

50 |

100% |

Figure

No 1.4:

The above sunburst

shows new opportunities that the NEP,2020 has presented for improving

accounting education. 80% of respondents answered "Yes" when asked

there any new opportunities that the NEP,2020 has presented for improving

accounting education 10% of respondents answered "No." Another 10% of

respondents answered "Maybe” there is new opportunities in accounting

education.

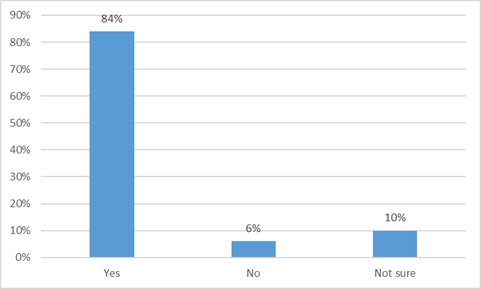

Section 4: Teaching and Learning Methods

5. Do

you believe the NEP,2020 encourages innovative teaching and learning methods in

accounting education?

Table

No 1.5:

|

|

Frequency |

Percent |

|

Yes |

42 |

84% |

|

No |

3 |

6% |

|

Not

sure |

5 |

10% |

|

Total |

50 |

100% |

Figure

No 1.5:

The above chart

shows teaching and learning methods in NEP. 84% educators believe that NEP,2020

encourages innovative teaching and learning methods in accounting education.10%

educators are not sure that NEP has brought

some changes in teaching learning methods. 6% educators are not in favor that

NEP has introduced any creativity.

6. Could

you provide examples of innovative teaching methods that have been implemented

or can be implemented in accounting education under the NEP,2020?

·

Suitable accounting standards framed,

conduct the research on the standards are important, frequently change the

standards and principles according to changes in the business patterns, results

will be analyzed and apply, give suggestions for better implementation of

industrial activities.

·

Demonstration method

·

Nothing implemented

·

Practical approach

·

By Visits to different Industries,

Companies we can Train them

·

No

·

Use of technology, games, group

discussions on business & economics etc.

·

Problem-Based Learning (PBL)

·

Case Studies and Simulations

·

Interactive Workshops and Seminars

·

Technology-Enhanced Learning

·

Flipped Classroom Approach

·

Peer Teaching and Collaborative Learning

·

Industry Internships and Experiential

Learning

·

Gamification

·

Research Projects and Case Analyses

·

Cross-Disciplinary Integration

·

Guest Lectures and Industry Expert

Sessions

·

E-Learning Platforms and Virtual

Classrooms

Section 5: Research and Development

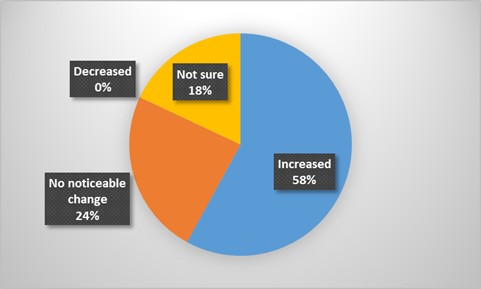

7. How

has the NEP,2020 impacted research initiatives in accounting education?

Table

No 1.6

|

|

Frequency |

Percent |

|

Increased |

29 |

58s% |

|

No noticeable change |

12 |

24% |

|

Decreased |

0 |

0% |

|

Not sure |

9 |

18% |

|

Total |

50 |

100% |

Figure

No 1.6

The above chart

shows how NEP, 2020 impact research initiatives in accounting education. 58% of

respondents reported that there has been an increase in their level of

awareness regarding the importance of environmental conservation. 24% of

respondents stated that they have not noticed any significant change in their

level of awareness. None of the respondents reported a decrease in their

awareness. 18% of respondents were unsure about the change in their awareness.

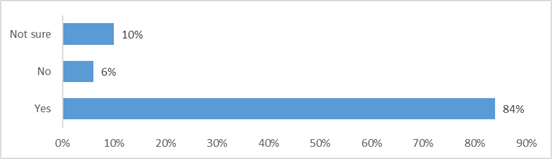

8. Are

there specific areas within accounting education that you believe require

further research attention under the NEP?

Table

No 1.7

|

|

Frequency |

Percent |

|

Yes |

42 |

84% |

|

No |

3 |

6% |

|

Not sure |

5 |

10% |

|

Total |

50 |

100% |

Figure

No 1.7:

The above chart shows specific areas within accounting education that

require further research attention under the NEP.

84% of respondents believe that there are specific areas within accounting

education that require further research attention under the National Education

Policy (NEP). Only 6% of respondents answered "No," indicating that

they do not believe further research is necessary. Additionally, 10% of

respondents were "Not sure." The total number of respondents is 50.

Section 6: Recommendations and Future Outlook

9.

What recommendations do you have for

policymakers, educators, and institutions to enhance accounting education in

light of the NEP,2020?

·

Students should get those understanding so

that they can work on accounting like tally software.

·

Reduce the syllabus so that students can

be through with given topics

·

Some concepts not related to present

situations. So frame curriculum as per the requirements

·

Research Methodology

·

Practicability

·

Educators

·

Create awareness on the career

opportunities in Commerce field. Industry experts need to be called in the

schools.

·

Align Curriculum with Industry Needs

·

Regularly review and update the accounting

curriculum to ensure it reflects current industry practices, emerging

technologies, and evolving regulatory requirements.

·

Engage with professionals and experts from

the accounting field to gather input on necessary skill sets.

·

Promote Experiential Learning

Opportunities

·

Encourage internships, apprenticeships, and

practical training in accounting firms, corporations, and financial

institutions. These experiences provide students with real-world exposure and

help bridge the gap between theory and practice.

·

Integrate Technology and Digital Literacy

·

Incorporate the use of accounting software,

data analytics tools, and other technological resources into the curriculum.

·

Provide training to both students and

educators to ensure proficiency in digital tools relevant to accounting.

·

Emphasize Critical Thinking and

Problem-Solving Skills

·

Design assignments, projects, and assessments

that require students to analyze complex financial scenarios, make informed

decisions, and solve accounting-related problems.

·

Encourage a culture of inquiry and

analytical thinking.

·

Foster a Multidisciplinary Approach:

Encourage collaboration between accounting departments and other disciplines

like finance, economics, law, and technology. This fosters a broader

understanding of business and financial concepts, aligning with the NEP's

multidisciplinary focus.

·

Incorporate Ethical Considerations and

Professional Values

·

Integrate discussions on ethical dilemmas,

professional conduct, and corporate governance into the curriculum.

·

Encourage students to think critically about

ethical issues in accounting practice.

·

Provide Continuous Professional

Development for Educators

·

Offer training and workshops for accounting

educators to keep them updated on industry trends, teaching methodologies, and

technological advancements. This ensures that educators are well-equipped to

deliver high-quality instruction.

·

Facilitate Research and Innovation in

Accounting Education: Encourage faculty and students to engage in research

projects related to accounting education. Support initiatives that explore

innovative teaching methods, assessment practices, and educational

technologies.

·

Promote Inclusivity and Accessibility

·

Implement policies and practices that ensure

equal access to accounting education for students from diverse backgrounds.

·

Provide support systems for students who

may face barriers to participation.

·

Offer Flexible Learning Pathways

·

Provide options for flexible course

scheduling, online learning, and part-time programs to accommodate the needs of

a diverse student population. This supports lifelong learning and accessibility

for working professionals.

·

Foster Industry Partnerships and Guest

Lectures

·

Collaborate with accounting firms,

corporations, and industry associations to provide guest lectures, workshops,

and networking opportunities. This exposes students to real-world professionals

and environments.

·

Evaluate and Monitor Outcomes so that

regularly assess the effectiveness of accounting education programs in

achieving learning outcomes and career readiness.

·

Use feedback from employers, alumni, and

industry stakeholders to inform continuous improvement efforts.

10. How

do you envision the future of accounting education in your country, considering

the influence of the NEP,2020?

·

Holistic and Multidisciplinary Approach

·

Emphasis on Practical Application

·

Technology Integration

·

The NEP

encourages experiential learning. In accounting education, this could mean more

hands-on activities, case studies, and simulations to apply theoretical

knowledge to real-world situations.

·

Accounting education is likely to become more

holistic, integrating knowledge from related fields like finance, economics,

law, and technology. This multidisciplinary approach will provide students with

a broader understanding of the business environment.

·

There will likely be a greater emphasis on

incorporating technology into accounting education. This includes using accounting

software, data analytics tools, and other technology platforms to prepare

students for the digital demands of the profession.

·

Critical Thinking and Problem-Solving Skills

·

The NEP's focus on critical thinking and

problem-solving will translate into accounting education.

·

Students will be challenged to analyze financial

data, make informed decisions, and address complex accounting issues.

·

Educators may adopt more innovative approaches, such

as flipped classrooms, interactive workshops, and collaborative learning, to

engage students and promote deeper understanding.

·

Innovative Teaching Methods

·

Ethical Awareness and Professional Values

·

Flexibility

in Learning Pathways

·

There will likely be an increased emphasis on

instilling ethical awareness and professional values in accounting education,

aligning with the NEP's goal of producing responsible and ethical citizens.

·

The NEP supports flexible learning options.

Accounting education may become more adaptable, offering online courses,

part-time programs, and alternative pathways to accommodate diverse student

needs.

·

Continuous Professional Development for Educators

·

Accounting

educators may receive more support and opportunities for professional

development to stay updated on industry trends, teaching methodologies, and

technological advancements.

·

Research and Innovation in Accounting Education

·

There may be

a surge in research initiatives focused on improving accounting education, including

studies on effective teaching methods, assessment strategies, and the impact of

technology integration.

·

Global Perspective in Accounting Curriculum

·

With an increasingly globalized business

environment, accounting education may incorporate international accounting

standards, global business practices, and cross-border financial reporting

considerations.

·

Inclusive and Accessible Education

·

Efforts to

ensure inclusivity and accessibility in accounting education may be further

emphasized, aiming to provide equal opportunities for students from diverse

backgrounds.

·

Outcome-Oriented Education so that there may be an

increased emphasis on measuring learning outcomes and preparing students for

successful careers in accounting, with a focus on employability and practical

skills.

CONCLUSION

In conclusion, this analysis delves into the

intersection of Accounting Education and the National Education Policy,2020

aiming to understand the implications of the policy on the field of accounting

education. The National Education Policy of 2020, with its emphasis on

multidisciplinary, experiential learning, and technology integration, presents

a transformative framework for education in India.

Within the realm of accounting education, these

policy reforms hold significant promise. The emphasis on vocational education

and the integration of practical skills alongside theoretical knowledge

addresses a longstanding need in the field. Moreover, the policy's focus on

research and innovation aligns with the dynamic nature of accounting standards

and practices, encouraging educators and professionals to contribute to the

evolving landscape.

The encouragement of ethical values and

professionalism in education resonates deeply with the ethos of the accounting

profession. Instilling these principles from the foundational stages of

education can contribute to a culture of integrity and responsibility within

the accounting community.

However, as with any policy implementation,

challenges and nuances will undoubtedly emerge. It will be imperative for

educators, policymakers, and practitioners to collaborate in navigating these

complexities, ensuring that the policy's vision translates into tangible

benefits for accounting education.

Looking forward, the successful integration of the National

Education Policy into accounting education has the potential to produce a new

generation of accounting professionals who are not only technically adept but

also possess critical thinking skills, ethical awareness, and a global

perspective. As the policy takes root and evolves, it is poised to shape a

brighter future for accounting education in India.

SCOPE FOR FUTURE RESEARCH

Conduct a longitudinal study to track the long-term

impact of the NEP,2020 on accounting education in India, considering factors

such as curriculum changes, teaching methodologies, and student outcomes over

time. Compare the effectiveness of accounting education under the NEP,2020 with

previous education policies to assess improvements and areas of concern.

Investigate the perspectives of other stakeholders such as students, employers,

and policymakers to gain a comprehensive understanding of the implications of

the NEP,2020 on accounting education. Explore the impact of the NEP,2020 on the

employability and career outcomes of accounting graduates, including their

readiness for the workforce and alignment with industry needs. the

effectiveness of technology integration in accounting education under the

NEP,2020, including the adoption of accounting software, data analytics tools,

and online learning platforms. Examine efforts to promote inclusivity and

accessibility in accounting education under the NEP,2020, focusing on

addressing barriers faced by marginalized communities and promoting equal

opportunities for all students. Investigate the challenges encountered in the

implementation of the NEP,2020 in the context of accounting education,

including issues related to infrastructure, resource allocation, and

stakeholder engagement.

REFERENCES

1.

National Education Policy 2020, Ministry

of HumanResource Development, Govt. of India. https://www.education. gov.

in/sites/ upload_files /mhrd/files/ NEP_Final_ English_0. pdf.

2.

Aithal, P. S., &Aithal, S. (2020).

Analysis of the Indian National Education Policy 2020 towards Achieving its

Objectives. International Journal of Management, Technology, and Social

Sciences (IJMTS), 5 (2), 19-41.

3.

Jha, P., &Parvati, P. (2020). National

Education Policy, 2020. (2020). Governance at Banks, Economic & Political

Weekly, 55 (34), 14-17.

4.

Braun, V., & Clarke, V. (2006). Using

thematic analysis in psychology. Qualitative Research in Psychology, 3(2),

77-101.

5.

Holloway, I., & Galvin, K. (2016).

Qualitative Research in Nursing and Healthcare. John Wiley & Sons. Aithal,

P. S., &Aithal, S. (2019). Analysis of Higher Education in Indian National

Education Policy Proposal 2019 and Its Implementation Challenges. International

Journal of Applied Engineering andManagement Letters (IJAEML), 3 (2), 1-35.

6.

Sunil Kumar Saroha, &UttamAnand

(2020). New instruction procedure 2020 Highlights: To see huge movements in

schools and advanced edification. IOSR Journal of Humanities and Social Science

(IOSR- JHSS), 25 (8), 59-62.

7.

Singh, H., & Dey, A. K. (2020). Listen

to my story: contribution of patients to their healthcare through effective

communication with doctors. Health Services Management Research. https://

doi.org/10.1177/0951484820952308

8.

Smith, J., Bekker, H., Cheater, F. (2011).

Theoretical versus pragmatic design challenges in qualitative research. Nurse

Researcher, 18(2), 39– 51.

9.

Suryavanshi, S. (2020). Reflections from a

Comparative Study for Reimagining Indian Universities. UNIVERSITY NEWS, 58

(33), 96- 102.

10.

Kumar, K., Prakash, A., & Singh, K.

(2020). How National Education Policy 2020 can be a lodestar to transform

future generation in India. Journal of Public Affairs, 20 (4), e2500. https:

//doi. org/10.1002/pa.2500

11.

Nicholas J.

Paisey (2003), "An analysis of accounting education research in accounting

education: an international journal – 1992–2001"

12.

Deb, P. (2020),

"Vision for Foreign Universities in the National Education Policy 2020: A

Critique"

13.

Aithal (2020),

"Analysis of the Indian National Education Policy 2020 toward Achieving

its Objectives"

14.

Ponemon,

Lawrence; Glazer, Alan (2021), "Accounting Education and Ethical

Development: The Influence of Liberal Learning on Students and Alumni in

Accounting Practice"